Building the truth machine

We are getting much better at predicting the future. AI forecasting systems are climbing leaderboards that were once the exclusive domain of elite human “superforecasters”—and they may soon surpass us at divining the trajectory of our messy, contingent world. Developments in AI dangle the tantalizing prospect that, some day, we might actually be able to see what’s coming next with increasing precision.

Prediction markets are the coordinating layer; they attract information by offering monetary rewards to those with useful information about the future. They promise to be platforms where millions of people—and increasingly, AI agents—put real money behind their beliefs about what’s going to happen, generating live probability estimates on everything from Federal Reserve decisions to legislative outcomes.

The vision is powerful. Kalshi CEO Tarek Mansour calls his platform a “truth machine,” arguing that “people don’t lie with their money” and that prediction markets are “replacing debate and subjectivity with markets and accuracy.” Polymarket CEO Shayne Coplan says much the same, positioning his platform as a “global truth machine” and telling the Wall Street Journal he expects billions of people will eventually use it, with its data informing government policy and becoming a go-to source for verifying information.

As I’ve written about before, I find this vision genuinely compelling. Much of our lives are about making decisions under uncertainty. Information helps us make better decisions. And prediction markets—where individuals, freely pursuing their own incentives, generate a public good in the form of a clearer shared picture of a complex world—represent a fascinating mechanism for the digital era.

But we still have serious work to do to achieve this grand vision.

The central problem is that the political and policy markets—those arguably most core to the social value proposition of prediction markets—are mostly ghost towns today.

The empty floor

To uncover this, Elliot Paschal and I have spent the last six months building a unique dataset. We started by pulling all Polymarket and Kalshi markets, historical to present, and then filtered them down to only those that pertain to politics. Then, for American election contracts, we went contract by contract and tried to find all those that both platforms listed, vs. all those that were only on one platform or the other—data that, so far as we know, no one else has put together.

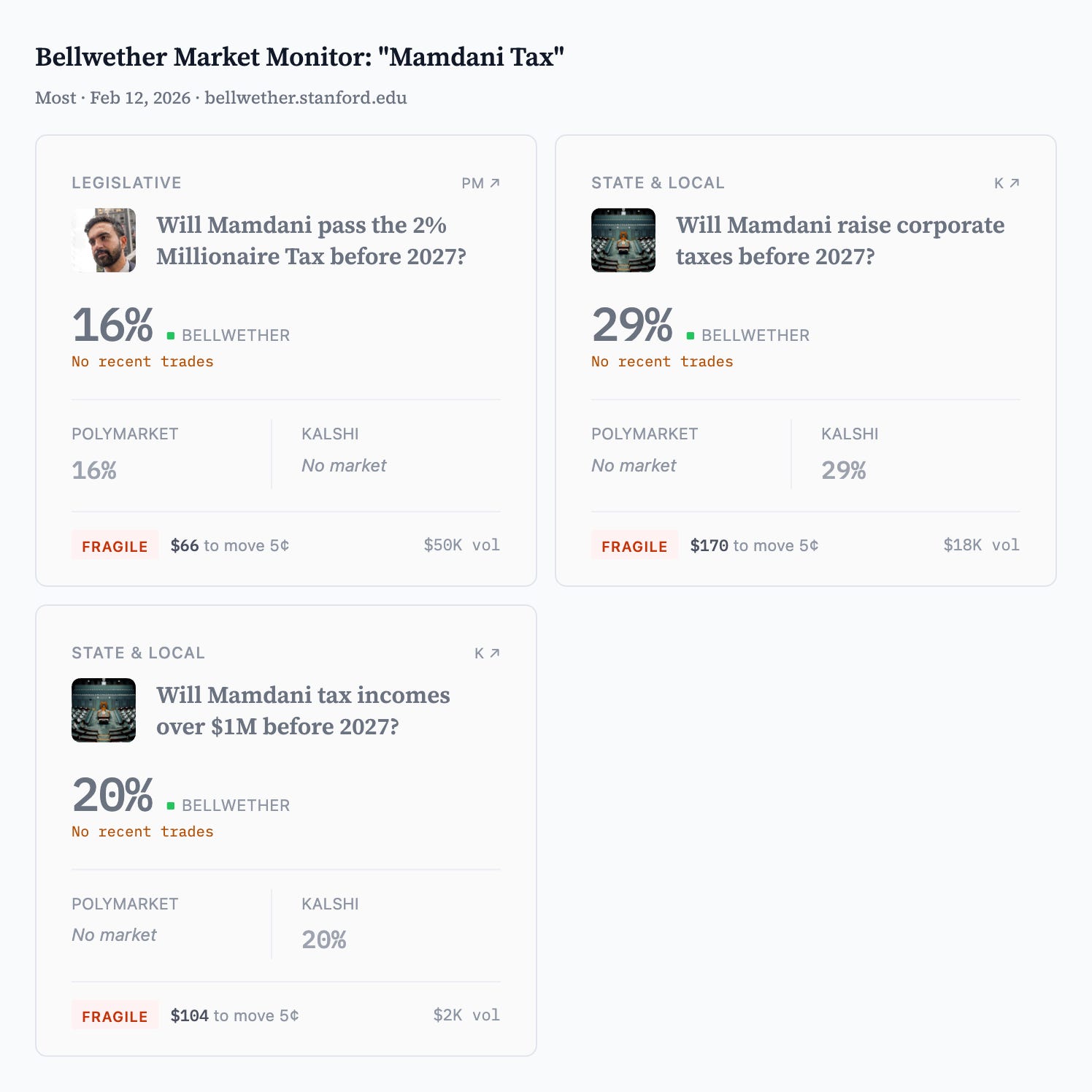

Consider a question that matters to millions of people right now: will New York’s new mayor, Zohran Mamdani, raise corporate taxes? He traveled to Albany this week to pitch lawmakers on hiking the combined corporate rate to over 22% and adding a 2% surcharge on millionaires. Governor Hochul has expressed misgivings but left the door open on corporate rates.

Whether any of this passes matters enormously for businesses in New York and for the city’s fiscal trajectory. Suppose you’re a business owner in the city. You’re planning out your budget for the next year. Should you staff up to meet anticipated growth in your business? Or save up money to cover an expected new tax burden? It would be awfully nice to have an accurate estimate of the expected tax rate for next year as you make decisions like these. You probably don’t want punditry or idle speculation—you’d probably much rather have concrete probabilities derived from traders putting their money where their mouth is.

But can you? A Kalshi contract asks: “Will Mamdani raise corporate taxes before 2027?” It has less than $30,000 in total volume. A somewhat related though different Polymarket contract on the possibility of a millionaire tax has less than $50,000, almost no liquidity, and therefore no way for an informed trader to profitably participate.

Our new research shows that this pattern is the norm, not the exception. For most political events, there’s very little money at play. Compounding this issue, the two dominant prediction markets don’t offer the same contracts, fragmenting this scarce liquidity even more. And of course, there are many other potentially valuable political events for which no contract is listed at all.

Prediction markets and politics: our diagnosis

We’ve put this all into a living research project available on the web—currently, it’s in beta, so please give us feedback—which serves as a live tracker of the strength and value of current prediction-market prices for understanding politics.

From this new research, we’ve documented three interesting findings about political contracts on Kalshi and Polymarket.

Finding 1: The markets that matter most are the markets nobody’s in.

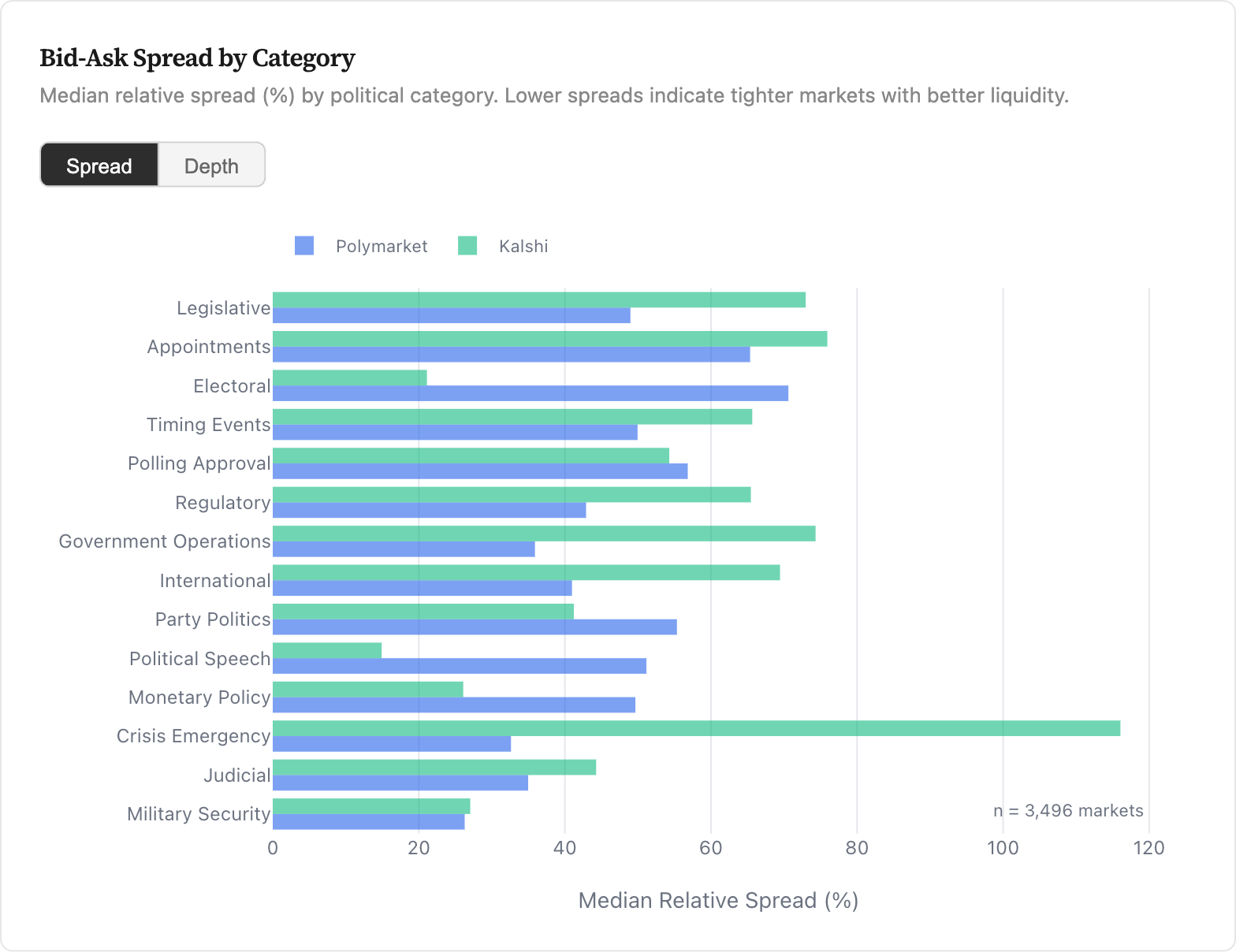

For the vast majority of political contracts, there’s almost no one on the other side of the trade. One way to see this: the gap between what buyers are willing to pay and what sellers are asking—a standard measure of how active a market is—typically exceeds 20% of the midpoint price, and is often much higher than that. That’s enormous. In a healthy, liquid market, that gap is no more than a few percentage points at most.

Interestingly, it’s not the case that less liquid markets are necessarily less accurate at predicting outcomes. Sometimes markets stay illiquid precisely because they’re already accurate, and there’s no incentive for new money to enter. Even quite small prediction markets have historically shown strong predictive performance—Wolfers and Zitzewitz documented accurate forecasts from markets with as few as 20 to 60 participants. More recently, Clinton and Huang’s analysis of over 2,500 political contracts from the 2024 election found that PredictIt—the most restricted platform, with position limits of just $850 per contract—correctly predicted 93% of outcomes, compared with 78% for Kalshi and 67% for Polymarket. Markets with more trading activity were not more accurate, controlling for the types of events being traded.

But thin markets are certainly cheaper to manipulate, as I have argued recently. When liquidity is low, a single motivated actor can move prices without anyone around to push back—and in a world where CNN and CNBC are now broadcasting these prices to millions of viewers, that vulnerability matters more than ever.

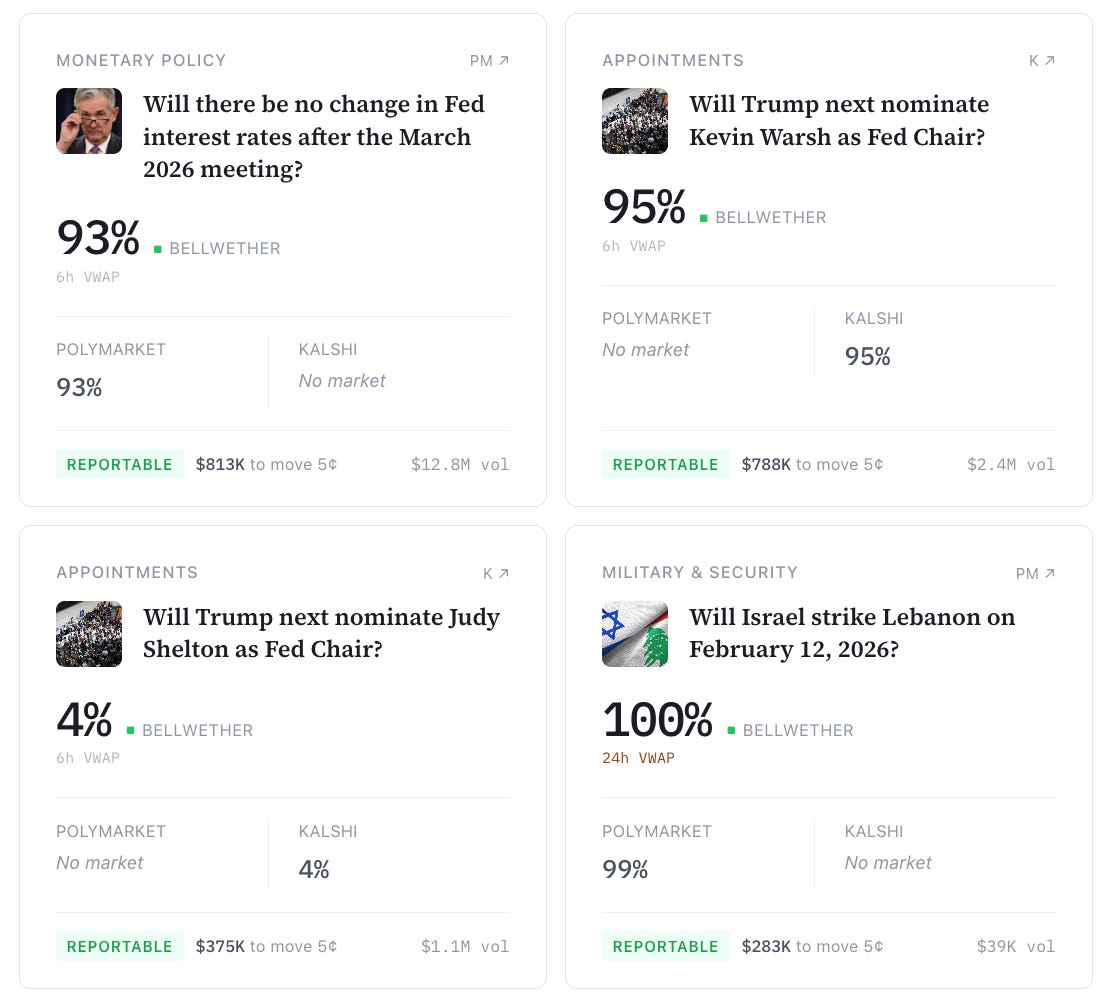

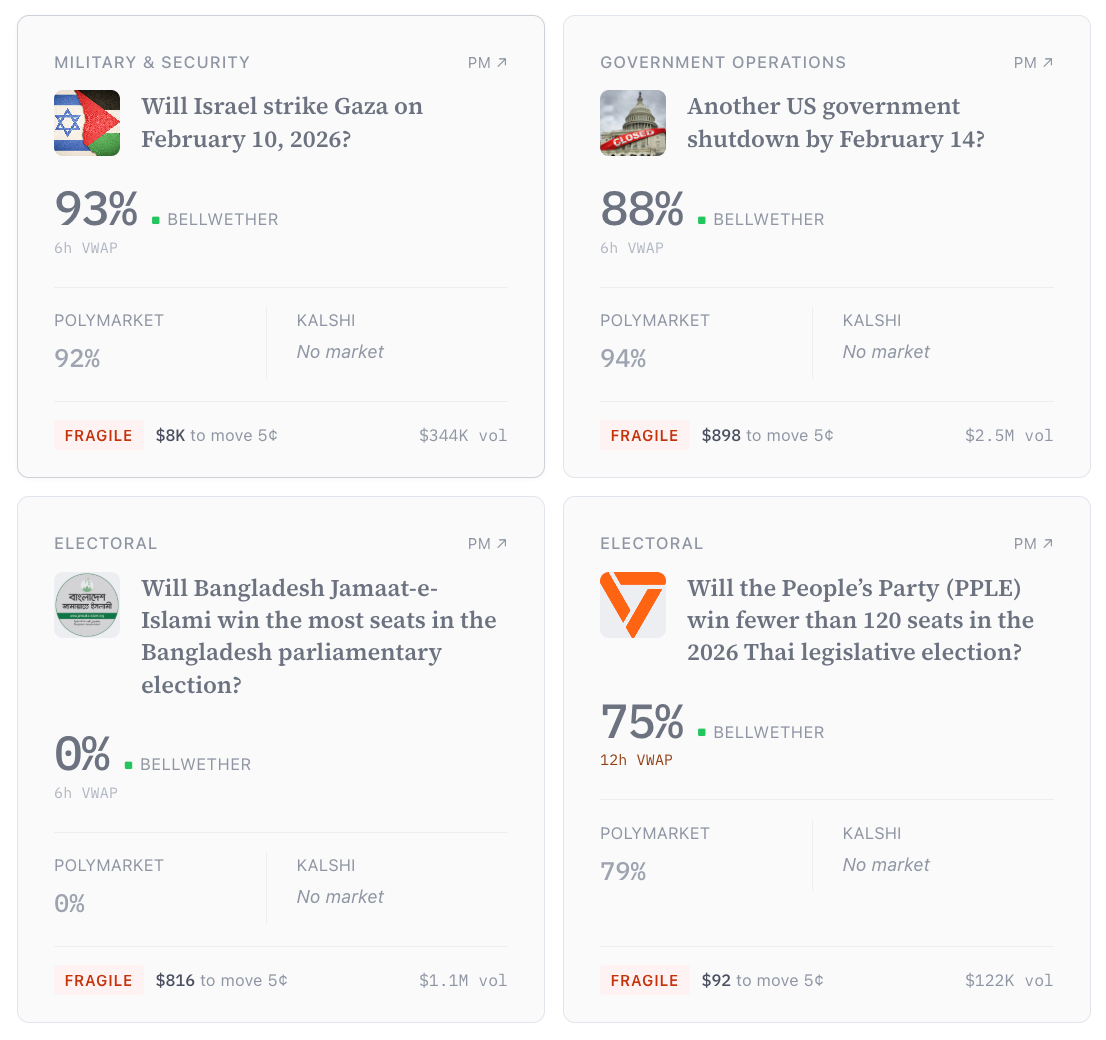

To visualize this, our dashboard estimates how much money a trader would have to spend to move the price by 5 cents (reflecting a 5 percentage-point change in the estimated probability of the event). When it’s cheap to move the price, we call this market “fragile”---and we recommend news outlets don’t report on it. When it’s expensive to move the price, we call it “reportable.” (These are only estimates, because sometimes traders have automated trades ready to go that don’t sit on the order book, but they still give a good indication of fragility.)

Based on this definition, we find that only 1.3% of all political markets listed on Kalshi and Polymarket are reportable today. Below are some examples of reportable and fragile markets.

Finding 2: Sharp on elections…fuzzy on most everything else.

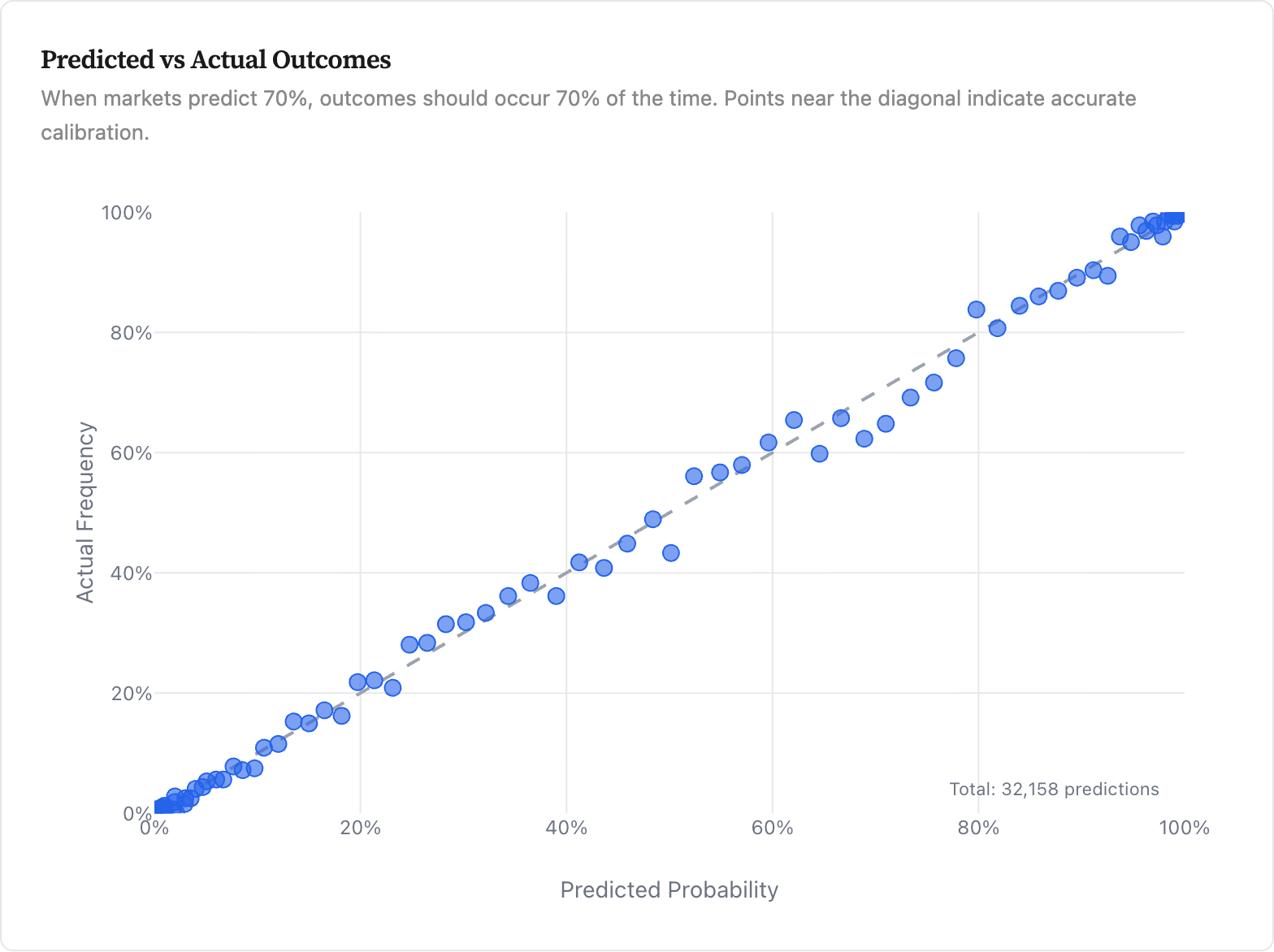

The good news: prediction markets are broadly predictive of political outcomes, as past research has found (including very recent work here and here). The figure below tests this directly: when the market says something has, say, a 70% chance of happening, does it actually happen about 70% of the time? For the most part, yes. The points cluster close to the line of perfect accuracy.

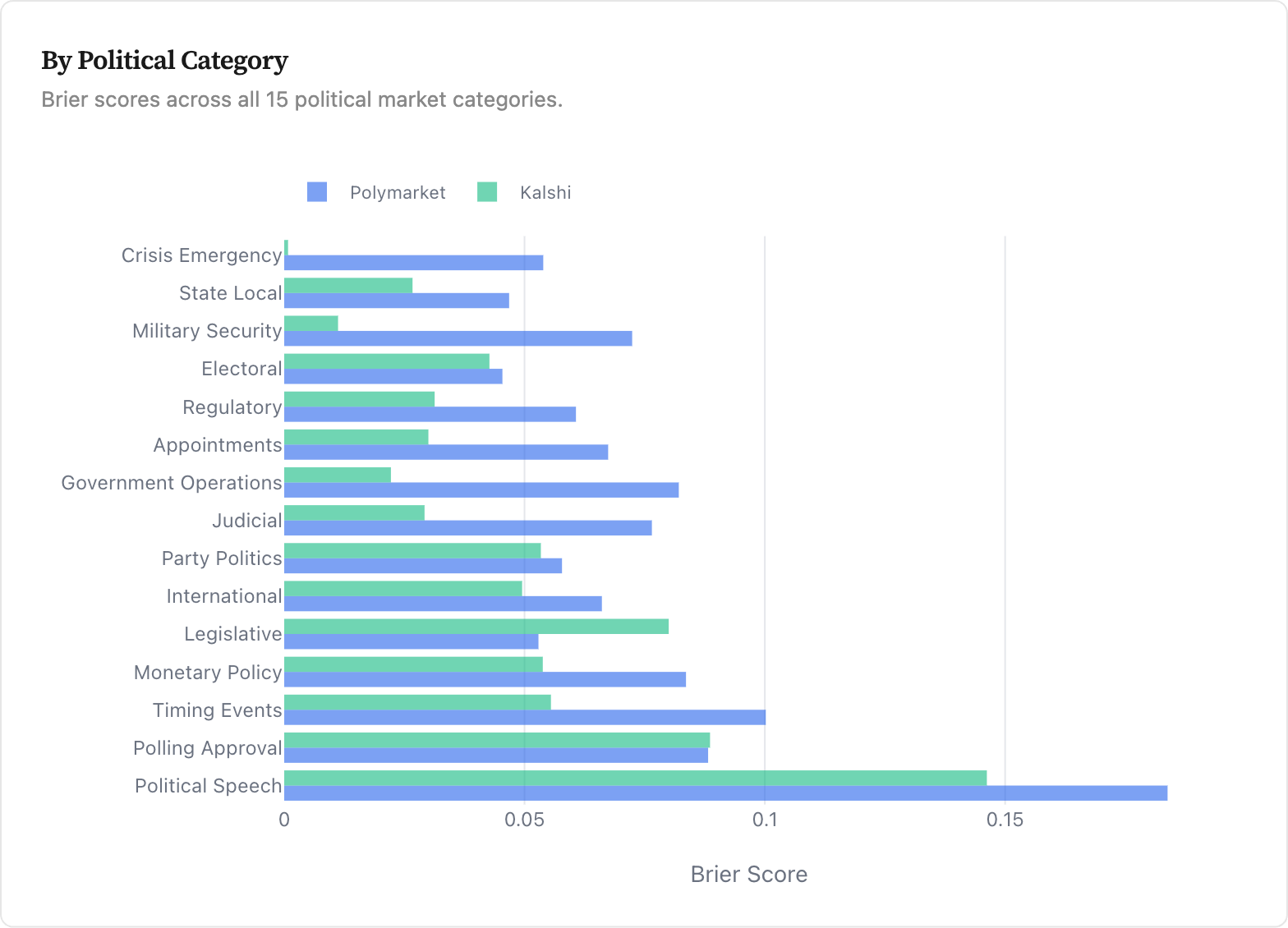

But this accuracy is uneven. The second chart breaks down how well Kalshi and Polymarket predict different types of political outcomes, using a standard accuracy measure, the Brier score (think of it like a golf score, where lower is better).

As the chart shows, within politics, their accuracy varies a lot. They’re generally solid at predicting elections, as well as some kinds of military security issues, state and local politics, and crises. They struggle with political speeches, which is not surprising since it’s a fundamentally hard and chaotic task. (They also struggle to predict polling approval, which may be in part a function of how those markets are structured.)

For most other outcomes that people care about, their performance is somewhere in the middle. This is not a criticism—for many of these outcomes, little other data exists, so prices are much better than nothing! But it is a limitation of the current approach.

Finding 3: The platforms are speaking different languages.

Kalshi and Polymarket rarely list the same political contract with the same rules. We can quantify this precisely for election markets, the most standardized contracts with identical resolution criteria (who wins). We examined this specifically for US election winner markets from 2024 through 2026. In this particular subset of contracts, only 70 of 131 resolved elections (53%) appeared on both platforms, and among 1,826 active electoral events, overlap drops to 18%. If fragmentation is this severe for elections, where the event is unambiguous, it’s almost certainly worse for fuzzier political contracts like legislation or geopolitical events.

This deters more efficient operating of the markets—it is hard to tell the difference between price gaps that are arbitrage opportunities vs. ones that indicate a delta in market expectations regarding resolution rules—and further fractures already thin liquidity.

A blueprint for building the truth machine

Mass consumer prediction market platforms are still quite new. Understandably, they’re focused first on creating sustainable businesses by exploiting product-market fit, which means listing a lot of contracts on things like sports. But if prediction markets are going to become the truth machines their founders promise, they need to work for the questions that matter most, not just the ones that generate the most volume.

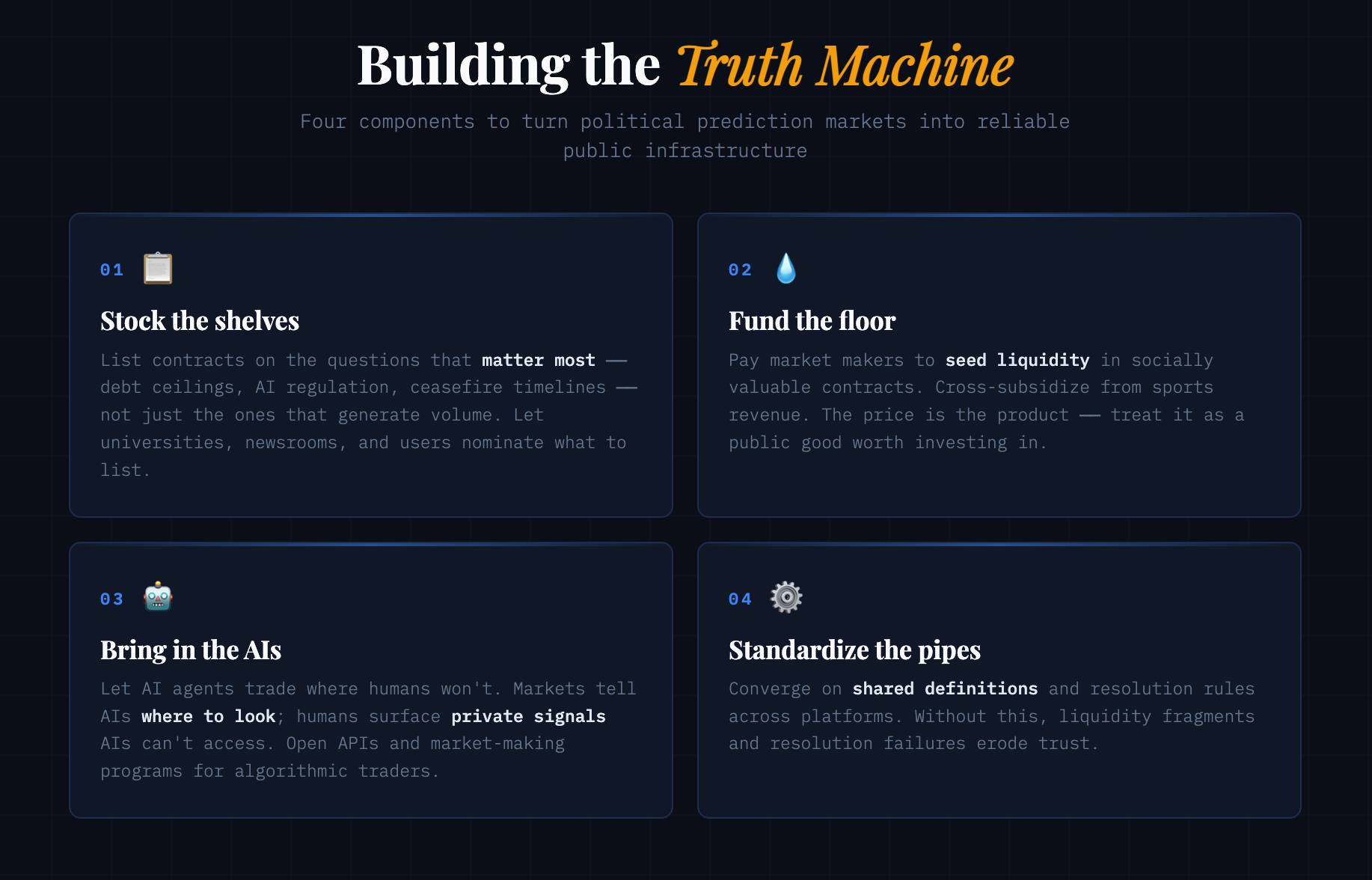

Building a truth machine requires four key components: questions worth answering, people willing to trade, intelligence capable of filling the gaps, and infrastructure reliable enough to trust. Right now, political prediction markets are missing most of these. Here’s how to fix that.

Stock the shelves

A truth machine is useless if it doesn’t cover the questions people need answered. Will Congress raise the debt ceiling before the deadline? Will a ceasefire hold? Will a specific piece of AI regulation pass? These are questions where millions of people — business owners, investors, policymakers — would benefit from a continuously updated probability estimate. And yet many either have no contract listed at all, or have one so thinly traded that the price is meaningless.

Beyond current events, there are deeper structural questions that prediction markets are uniquely positioned to address. What is the probability that AI displaces more than 10% of jobs in a given sector by 2030? What is the likelihood that a given state adopts ranked-choice voting? These are questions where conventional expert opinion is noisy, politicized, or both — precisely the conditions where prediction markets should add the most value.

Platforms can’t identify all of these on their own. Universities, think tanks, and news organizations that have already partnered with these platforms — CNN with Kalshi, the Wall Street Journal with Polymarket — could help flag the questions their audiences most need answered. Platforms could also let their own users propose and vote on which markets to list next, drawing on signals from the traders who’ve already shown interest in non-sports contracts.

Fund the floor

Listing the right questions is necessary but not sufficient. A truth machine needs traders on both sides of every contract — and for most political questions, the private incentive to trade is too small to get them there.

This is a public goods problem. The social value of a well-functioning prediction market on AI safety legislation or the next government shutdown is enormous. But no individual trader captures that value. The information that trading produces — the price — is a public good that helps everyone make better decisions. As Adhi Rajaprabhakaran writes: “the primary product of prediction markets isn’t the ability to trade. It’s the information that trading produces. The price is the product.”

Classic public goods require some form of subsidy, and prediction markets are no different. The most promising lever is paying market makers to provide liquidity in socially valuable markets — effectively seeding these ghost towns with enough activity that real trading can take hold.

Where does the money come from? The most natural source is cross-subsidy from the sports markets generating billions in volume today. A modest allocation toward political and policy markets isn’t charity — it’s the investment that justifies the “truth machine” narrative that differentiates these platforms from DraftKings.

Philanthropic and government funders like Open Philanthropy, Schmidt Futures, or IARPA — which has historically funded forecasting tournaments on questions of national security interest — could supplement this.

AI could trade where humans won’t—but we need markets to coordinate it

Even with better incentives, some valuable markets will struggle to attract human traders. This is where AI agents come in—-and where the truth machine metaphor starts to get literal!

As AI forecasting systems improve, a natural question arises: do we even need prediction markets at all? Why not just have AIs report forecasts directly?

Two reasons. First, markets tell AI agents where to look. The universe of possible questions is infinite. Should an AI spend its compute forecasting a government shutdown, semiconductor export controls, or a mayoral race? Without a price signal showing which questions are mispriced, even a highly capable AI is guessing about where to deploy its attention. Markets provide that signal — they’re the scheduling layer for AI intelligence, directing agents to the questions where their contribution is most valuable. This is the point Alex Imas and Rohit Krishnan have made: markets don’t just aggregate information, they coordinate the allocation of intelligence.

Second, markets surface information that AI simply can’t access. AI forecasters synthesize public data — news, historical patterns, data releases. But prediction markets can also incorporate harder to find information: the business owner who sees the economy shifting on the ground before it shows up in the data; the AI expert who notices a remarkable new capability in the model she’s using; the pollster whose new data indicates a political shift no one else has seen yet. Markets create a financial incentive for these people to reveal what they know by putting money behind it. No AI can replicate this, because the information doesn’t exist in any corpus it can reach.

The most valuable truth machines will combine both: AI-generated forecasts that are cheap, fast, and capable of synthesizing vast public data, alongside human intelligence that is expensive, slow, and capable of incorporating private signals that exist nowhere else. Platforms should actively encourage this — through open API access, reduced fees for algorithmic trading, and explicit market-making programs designed for AI agents.

Standardize the boring infrastructure that makes everything else work

This recommendation is the least exciting and perhaps the most important. Right now, Kalshi and Polymarket rarely list the same political contract with the same resolution rules. This matters more than it might seem.

We’ve seen what happens when this goes wrong. The recent dust-up over whether Cardi B danced at the Super Bowl half time show or not. The Zelensky suit debacle. The government shutdown contract on Polymarket that resolved based on when the OPM website was updated, not when the president signed the bill—causing traders who correctly predicted the political outcome to lose their bets to a bureaucratic delay. As I wrote in my piece on AI judges for prediction markets, these resolution failures don’t just cost individual traders money—they erode the trust that the entire system depends on.

These failures don’t just cost individual traders money. They erode the trust the entire system depends on. The fix is unsexy but essential: shared contract definitions across platforms. The financial industry did this decades ago with credit derivatives, when competing banks agreed on standard definitions and a common resolution process through the ISDA framework despite being fierce competitors. Prediction markets need their equivalent — agreed standards for what “passing a bill” or “winning an election” means, so that liquidity concentrates instead of fragmenting.

Without this, everything else in the blueprint breaks. You can list the right questions, fund the liquidity, bring in AI traders, and attract hedgers — but if the machine can’t agree on what’s true when the contract resolves, it’s not a truth machine at all.

Turn political markets into political risk insurance

If we get thick political markets organized around clear resolution rules, we can get the truth machine’s flywheel spinning. And there is an underappreciated force that can help it gain momentum: hedging against political risk.

Consider again the New York business owner worried about Mamdani’s corporate tax hike. If there were a liquid prediction market on the tax increase, she could buy “yes” shares as insurance — if it passes, the payout offsets some of the new burden; if it doesn’t, she’s out a small premium. She doesn’t need to be a forecasting genius. She just needs a hedge.

The perhaps counterintuitive part is that that business owner isn’t just protecting herself. She’s also providing the other side of the trade that makes it profitable for informed traders—and AI agents—to show up. Without hedgers, market makers sometimes face a market full of sharks and widen their spreads until nobody trades. Hedgers help sustain vigorous, liquid markets. This is a deep insight from Glosten and Milgrom’s foundational work on market microstructure: it is the presence of “liquidity traders”—people trading for reasons other than to exploit private information—that makes it profitable for informed traders to participate at all.

Right now, political prediction markets have almost no hedgers. Changing that could be transformative.

Conclusion

In a world where trust in media is at all-time lows, the promise of a truth machine based on objective prices is obvious. Rajiv Sethi has laid out this idea quite beautifully:

“Prediction markets play an interesting and usual role in this environment. They encourage people with opposing worldviews to interact with each other in anonymous, credible, and non-violent ways. In a sense, they are the opposite of echo chambers. A market with homogeneous beliefs would have no trading volume, or would attract those with different opinions who are drawn by what they perceive to be mispriced contracts.”

Today, prediction markets have a lot of momentum. . The sports volume is there. The AI is getting there. The opportunity now is to treat political prediction markets as public goods worth investing in, not just betting products worth monetizing. If we do, we might actually get the truth machine we’ve been promised.

Disclosures: In addition to my appointments at Stanford GSB and the Hoover Institution, I receive consulting income as an advisor to a16z crypto and Meta Platforms, Inc. My writing is independent of this advising and I speak only on my own behalf.

| A guest post by

|

Let's be real here: No one will use prediction markets to hedge risks. Binary options are poor instruments for hedging and have nearly no legitimate uses that could not be done better with existing instruments like futures or insurance contracts with linear payoffs. That's why binary options are illegal in much of the world. If someone wanted to hedge their tax risk with Mamdani, they would hedge it directly with a contract that scales payoffs based on incremental tax paid, rather than take an indirect yes/no bet on Mamdani winning. Contracts like these are already thickly traded and are the real prediction markets.

There will be no institutional volume in the prediction markets because they aren't actually useful compared to existing markets. Binary options are bad for hedging. People want to hedge risks directly, not on events that indirectly affect their risks. The truth machine you want has already been built. You just access it through Bloomberg terminals and phone calls with your derivatives dealer.

Prediction markets are federally sanctioned sports betting. That's all. It's that simple. There's no there, there. You're mistaking the tail for dog. The "truth machine" narrative is a smokescreen to cover the mass violation of state gambling laws. We should just be honest about this. That's the real "truth machine" here.

Linking a recent design I worked on that tries to minimize subsidies required for useful prediction markets - https://virajnadkarni.substack.com/p/two-uses-of-knowledge-in-society