AI’s TACO Trade

Governance by stock market means that Trump can probably only push Anthropic so far. Markets seem to be betting he won’t. And they may make future AI regulation complicated, too.

"You mean to tell me that the success of the program and my reelection hinge on the Federal Reserve and a bunch of fucking bond traders?"

—Bill Clinton, as reported by Bob Woodward

Last Friday’s news that Anthropic was pulling its most powerful AI model, Fable, from the market under severe pressure from the Trump Administration was earthshaking. Seemingly everyone has a take on what this means for regulating AI going forward, how we’re entering a new era of government control, and so on. But you know who has seemed oddly unmoved? The stock market.

After several years of letting AI rip, the Trump Administration now wants to control it—to make sure foreign adversaries aren’t able to use these tools, to mitigate potentially catastrophic security threats, and, probably, based on public comments from Pete Hegseth and others, to punish Anthropic and Dario Amodei personally.

Clearly, we’re heading into a new regulatory regime, one in which the federal government pre-reviews models and de facto licenses them (Trump’s EO from just two weeks ago explicitly rejected a licensing framework, yet Howard Lutnick’s letter to Anthropic specifically says that they will need to obtain a license).

Will this encourage the kind of impartial, reasoned process of model oversight many have been calling for? Or, as Dean W. Ball has argued, and as seems far more likely, will this process look far more ad hoc and personal?

With AI still far from the top issue in Americans’ minds (Hormuz still dominated the news agenda last Friday despite the Fable takedown), it’s unlikely the midterm elections will provide a mandate for a codified legislative solution to this problem, in the US at least.

Which probably means, like in many other Trump policy domains, it comes down in large part to the stock market. This is the famous “TACO trade”---short for Trump Always Chickens Out, which means that he will (almost) always reverse course on a major policy decision if the stock market freaks out enough.

The basic TACO trade occurs when you buy the dip that some of Trump’s actions cause, confident he’ll reverse course and the market will recover.

But the “second order” TACO trade happens when the markets shrug in the first place, anticipating in advance that Trump won’t stay the course. Geopolitically-driven selling has become progressively more muted over time in line with this trend.

AI now seems capable enough to pose genuinely important risks, and at the same time so central to economic growth that slowing it down might mean tanking the stock market, reducing investment in the compute buildout, and consequently slowing the economy.

The market has been attentive to other AI signals in the past. When DeepSeek released R1 in January 2025, fears about AI’s growth story wiped out historic sums in a single day. So why did the market largely shrug at Fable being shut down—the largely unexpected pullback of the most capable product in the most economically important industry? On paper, it seems surprising.

It’s impossible to prove, but from digging into the data, I think there is now an ongoing “second order” TACO trade happening in AI. The market isn’t reacting because it doesn’t believe Trump is going to slow down AI, even despite any personal wishes he and his team may have to harm Anthropic.

People aren’t talking about this TACO trade much in AI circles because the conversation is dominated by more legalistic discussions about the emerging regulatory environment. And it’s easy to miss it, because it’s “the dog that didn’t bark”---the media isn’t going to be excited to cover the story that Trump’s battle with Anthropic hasn’t moved markets—but it carries rather complex implications for governance at the frontier, and the market’s tolerance for slowing AI development.

It’s the economy, stupid – and the economy is AI, now

To see the TACO AI situation, you first have to appreciate the well-known fact that the fate of the American economy now rests largely in the hands of AI. While the rest of the world stagnates, America’s economy continues to be remarkably strong, largely thanks to AI. Some basic statistics that have been well documented, but are worth reinforcing:

The largest AI and technology companies were responsible for 53% of all S&P 500 gains in 2025, according to Goldman Sachs.

The “Magnificent Seven” alone are about 34% of the index, while the ten largest AI/cloud/chip companies are about 38%, according to State Street’s SPY holdings data.

AI-related investment categories (information-processing equipment, software, and R&D) accounted for roughly 93% of U.S. GDP growth in Q1 2026, contributing 1.49 percentage points of 1.6% annualized growth, according to the Bureau of Economic Analysis.

Microsoft, Amazon, Alphabet, and Meta alone are expected to spend roughly $635 billion on AI infrastructure in 2026, up from $383 billion in 2025 and just $80 billion in 2019, according to a Reuters report citing S&P Global estimates.

The combined valuation of SpaceX, OAI, and Anthropic recent and prospective IPO’s ($3.6 trillion) roughly equals the GDP of France

Slowing down AI means slowing down the economy

I’ve written previously that we’ll see a much more potent populist backlash to AI if we start to see substantial job loss due to AI.

But there’s an interesting converse to this, too: the Trump Administration is going to fight like hell to keep the economy ripping and the stock market high, and that means keeping AI ripping. It means keeping the datacenter and compute buildout ripping, and it means keeping the frontier labs rolling, producing better and better tokens that companies and people want to buy more and more of.

We might have many reasons we want to slow down or even pause AI development and the release of new AI models to the public.

But slowing down AI means slowing down the economy. The entire AI buildout is predicated on continuing growth in the demand for tokens. Goldman Sachs expects AI token consumption to rise 24x by 2030, to 120 quadrillion tokens per month.

Releasing newer, better models is an essential part of how that demand continues to rise. OpenAI describes its business as a flywheel in which more compute produces step-change gains in model capability, stronger models unlock better products and broader adoption, adoption drives revenue, and revenue funds the next wave of compute.

This all keeps the engine running for an administration that has staked a lot of its economic credibility on AI dominance. This creates a fundamental political tension for Trump, in that his actions against Fable help make a broader pause seem more plausible—which risks slowing down the economy.

Of course, Trump might be able to slow down Anthropic without slowing down AI as a whole. If Anthropic isn’t able to release higher-quality new models, maybe customers just switch to OpenAI, compute reallocates as needed, and the economy keeps on humming.

But it’s awfully risky. Anthropic is the single highest-revenue frontier lab, now, and it is deeply enmeshed in the broader AI economy. The company has secured roughly 3.5 gigawatts of next-generation Google TPU capacity through Broadcom, beginning in 2027, while keeping Amazon as its primary cloud and training partner. Meanwhile, Google has separately committed to invest up to $40 billion in the company.

Slow Anthropic down and you may just threaten the financial plans of Broadcom, Alphabet, and Amazon…and countless others who exist in this network of economic dependencies.

The market is betting on an AI TACO

So is Trump going to slow Anthropic down? Might he even expand the approach and slow the other labs down, too? On a livestream with Nathan Labenz and Prakash this week, Liron Shapira argued that people who want to see a pause or slowdown in AI development should see Trump’s actions as a positive step towards that. I think there’s a lot for that line of argument. But markets don’t seem to think that’s where we’re headed.

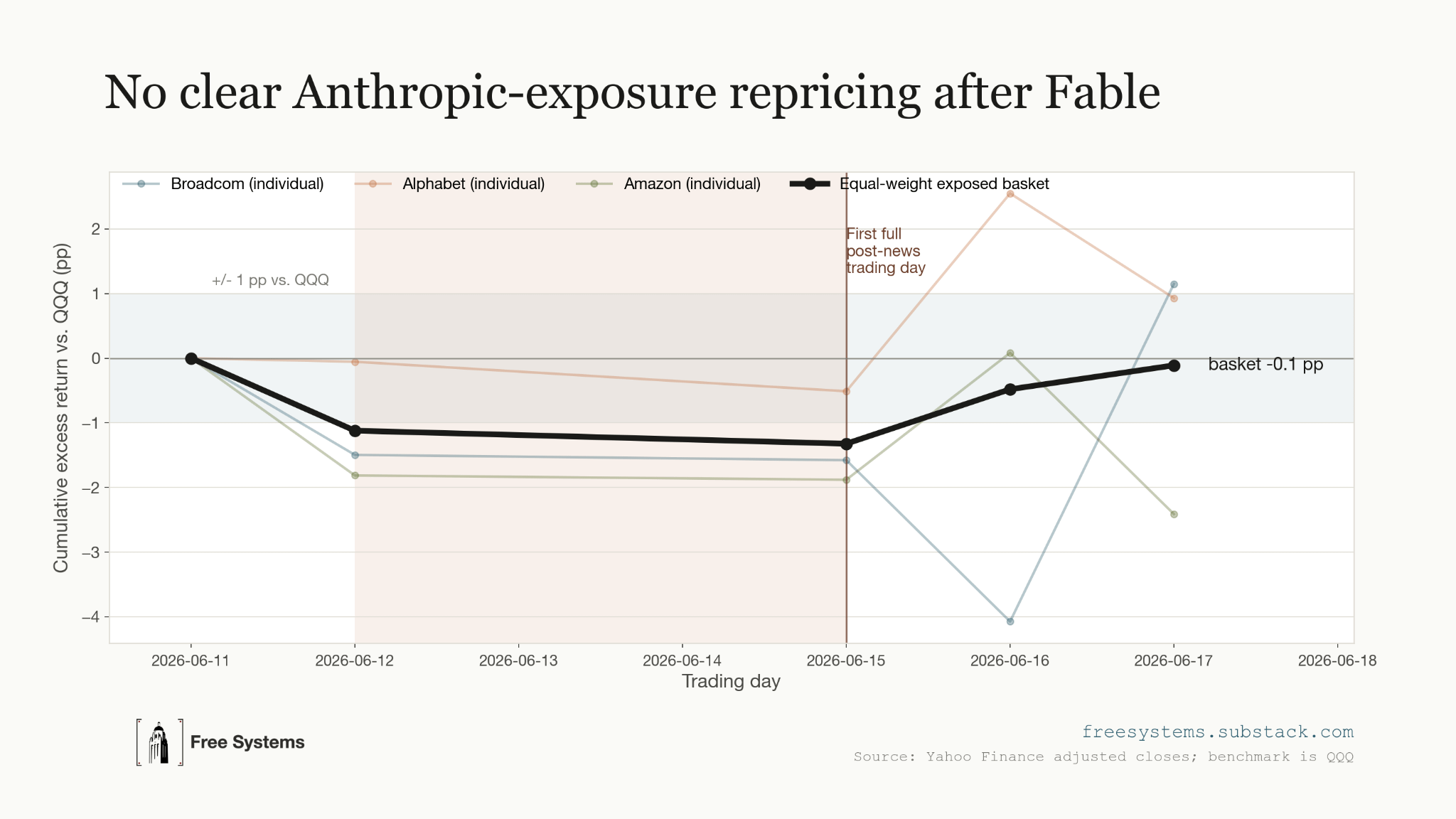

Squint at the returns of AI-exposed stocks around June 12th, when Fable went dark, and it’s hard to see a market reading the action as bad news for future AI earnings—though we should always keep in mind that since stock market prices have many determinants, this is hardly a clean test of how the Fable shutdown really affected investor sentiment.

The publicly traded names enmeshed with Anthropic, from Broadcom to Alphabet to Amazon, showed no such distress; in the first full session after the order they traded up alongside a market that happened to be rallying on unrelated news of a U.S.–Iran deal to reopen the Strait of Hormuz.

Remember, Nvidia’s stock plummeted by 16%, with Broadcom, Amazon and Microsoft’s prices all sinking too after DeepSeek’s model performance cast that, in some ways, also cast doubt on the certainty of the AI development buildout.

The clearest negative reaction showed up in Anthropic’s own pre-IPO proxies, where the Hyperliquid valuation perpetual slipped about 3.7%---not a huge amount, albeit in a strange and not that liquid market.

Meanwhile, over on Kalshi, traders are betting on a quick reversal rather than a long freeze: by mid-June they put the odds of Fable returning before July 1 at roughly 58%, and about 74% by July 10—a delay that will feel agonizing to those of us who fell in love with the model during our brief but glorious time with it, but nothing like the six-to-twelve-month slowdown that might really spook people.

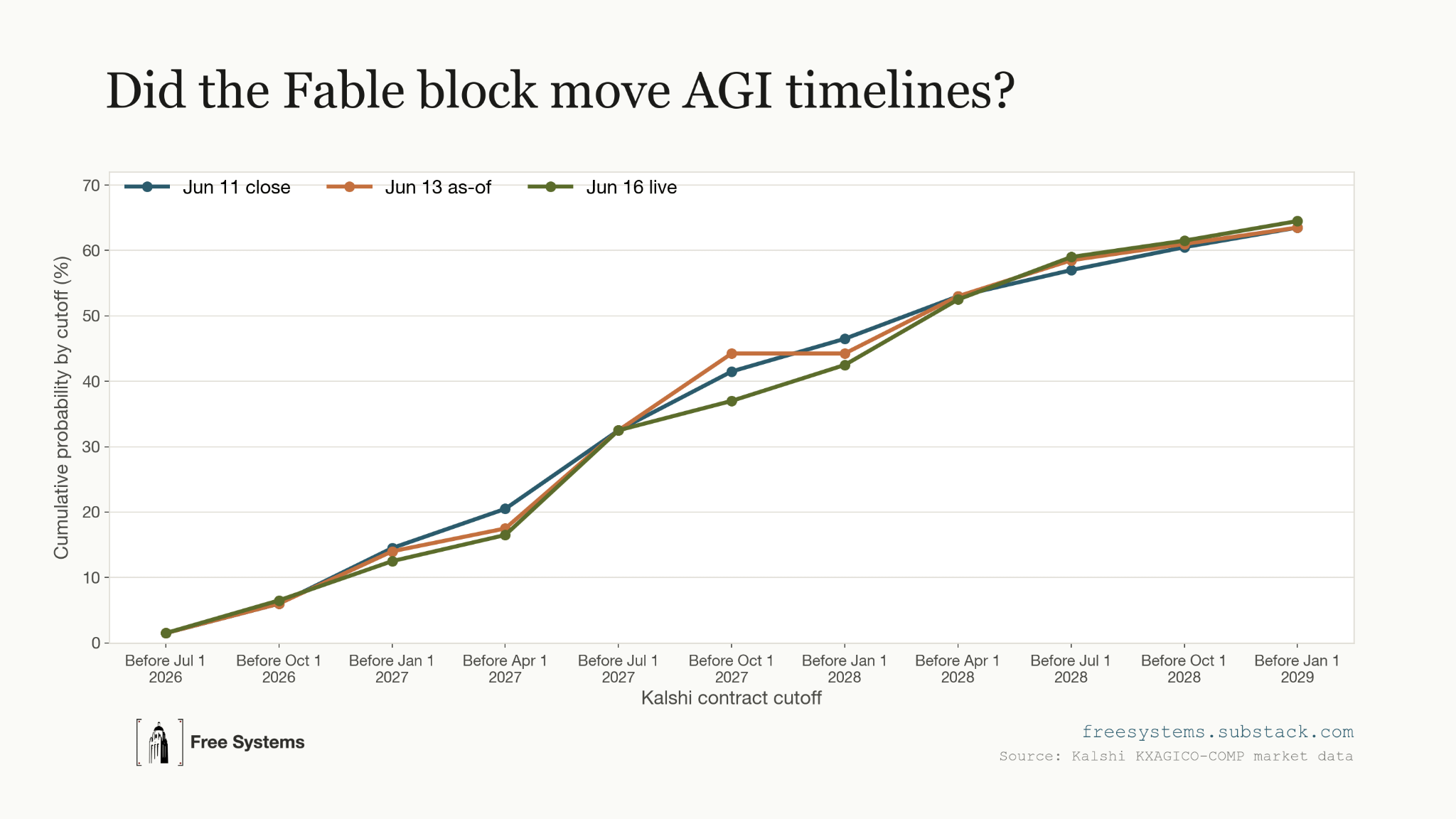

According to another Kalshi market, pulling Fable did slow down our expected timeline to a public lab announcement of attaining AGI…but only quite modestly.

As the figure below shows, the market adjusted down the chance that AGI is declared publicly by April 1st, 2027 by about 5 percentage points, and adjust down the chance it’s declared by Oct 1st, 2027 by another 5 points or so—reallocating that 10 percentage points of probability out to the post July 1st, 2028 period. These are pretty modest shifts.

Each of the above market signals could be interpreted a variety of ways. We can never conclusively prove if a second-order TACO trade is occurring or not. But there are some basic, hard facts we should keep in mind: the US economy is very dependent on AI, and taking any actions that risks slowing down the compute-revenue flywheel is inherently risky.

Trump’s actions on Fable have kicked off a thousand talking heads abuzz with the possibilities for how he might slow down AI progress. Meanwhile, Wall Street shrugs, and prediction markets tell us to expect Fable to return soon and progress towards AGI to continue largely apace.

What will be enough to give the stock market pause?

All this means we may be heading towards an impossible political bind. Nothing is more important to American voters than the state of the economy. And today, the economy rests on AI. We have to keep feeding the beast, maintaining expectations about future AI growth.

At the same time, we might have very serious cybersecurity and national security reasons to want to feed that beast a little bit more slowly. But with each passing day, the political costs of slowing down may rise, as AI becomes “too big to fail.” And this isn’t just a Trump story. If and when the Democrats take control of Congress in November, they too may discover that their enthusiasm to regulate AI more aggressively becomes tempered by a fear of being seen as responsible for crashing the stock market.

Or, maybe there’s a middleground. Maybe the market will reward prudent actions that reduce cybersecurity risks while allowing for AI development to proceed at a reasonable pace. This is really the big question for AI regulation: what kinds of regulatory steps will the market tolerate, and which will cause it to freak out? So far, Trump’s forays into tighter control over AI haven’t spooked the market, but it’s hard to know whether that’s because the market wants more regulation, or because the market thinks Trump won’t actually do it.